The call usually comes first. Then the mail starts arriving. A mortgage statement shows up at your parent's condo in Aventura, or a single-family house in Pembroke Pines, and suddenly grief turns into logistics.

If you're dealing with what happens if you inherit a house with a mortgage, the first point to understand is simple. The loan usually doesn't disappear when the owner dies. The house can still be kept, sold, or surrendered, but someone has to make decisions quickly, especially in Miami-Dade and Broward where vacant-property insurance issues, HOA pressure, and probate delays can become expensive fast.

This is manageable. But it is not passive. Families who do well with inherited Florida property usually move early on the lender, the insurance carrier, the HOA or condo association, and the probate filing.

Table of Contents

- An Heir's First Notice The Inherited Mortgage Bill

- Your First 30 Days Immediate Financial Obligations

- Understanding Your Legal Rights with an Inherited Mortgage

- How Florida Probate Impacts the Inherited House

- Decision Framework Keep Sell or Walk Away

- The Fast-Track Solution Selling Your Inherited House for Cash

- FAQ Inherited Mortgage Questions Answered

An Heir's First Notice The Inherited Mortgage Bill

The first mortgage bill after a death rattles most families because it raises two fears at once. Will the bank take the house, and am I now personally responsible for the debt? In Florida, those are separate questions, and treating them separately keeps you from making bad decisions under pressure.

In practice, the inherited property usually lands in one of three buckets. The loan is affordable and someone wants to keep the home. The house needs to be sold to pay the mortgage and close out the estate. Or the numbers are bad enough that the family needs to consider walking away from the property itself rather than sinking cash into it.

At a Glance

- The mortgage usually survives: The debt remains attached to the property, so the lender still expects payment.

- The clock starts immediately: Missed payments, unpaid insurance, tax delinquencies, and HOA balances can all complicate probate.

- Florida adds local friction: In Miami-Dade and Broward, condo and HOA communities often move faster than heirs expect on violations, access issues, and account freezes.

- Probate controls authority: Until the right person has legal authority, even basic decisions can stall.

- You still have options: Keep the house, sell it conventionally, sell it as-is, or in some cases decline to keep the property.

Practical rule: Treat an inherited mortgaged house like an active business asset for the first month. Sentiment matters, but deadlines matter more.

A lot of generic advice stops at “assume the loan or sell.” That isn't enough in South Florida. You also need to think about vacancy, roof age, water intrusion, windstorm coverage, association estoppels, and whether the personal representative can access documents in time.

The right approach is direct. Confirm who has legal authority. Stabilize the carrying costs. Figure out whether the house has equity, deferred maintenance, or title issues. Then decide whether keeping it still makes sense once actual costs are on paper.

Your First 30 Days Immediate Financial Obligations

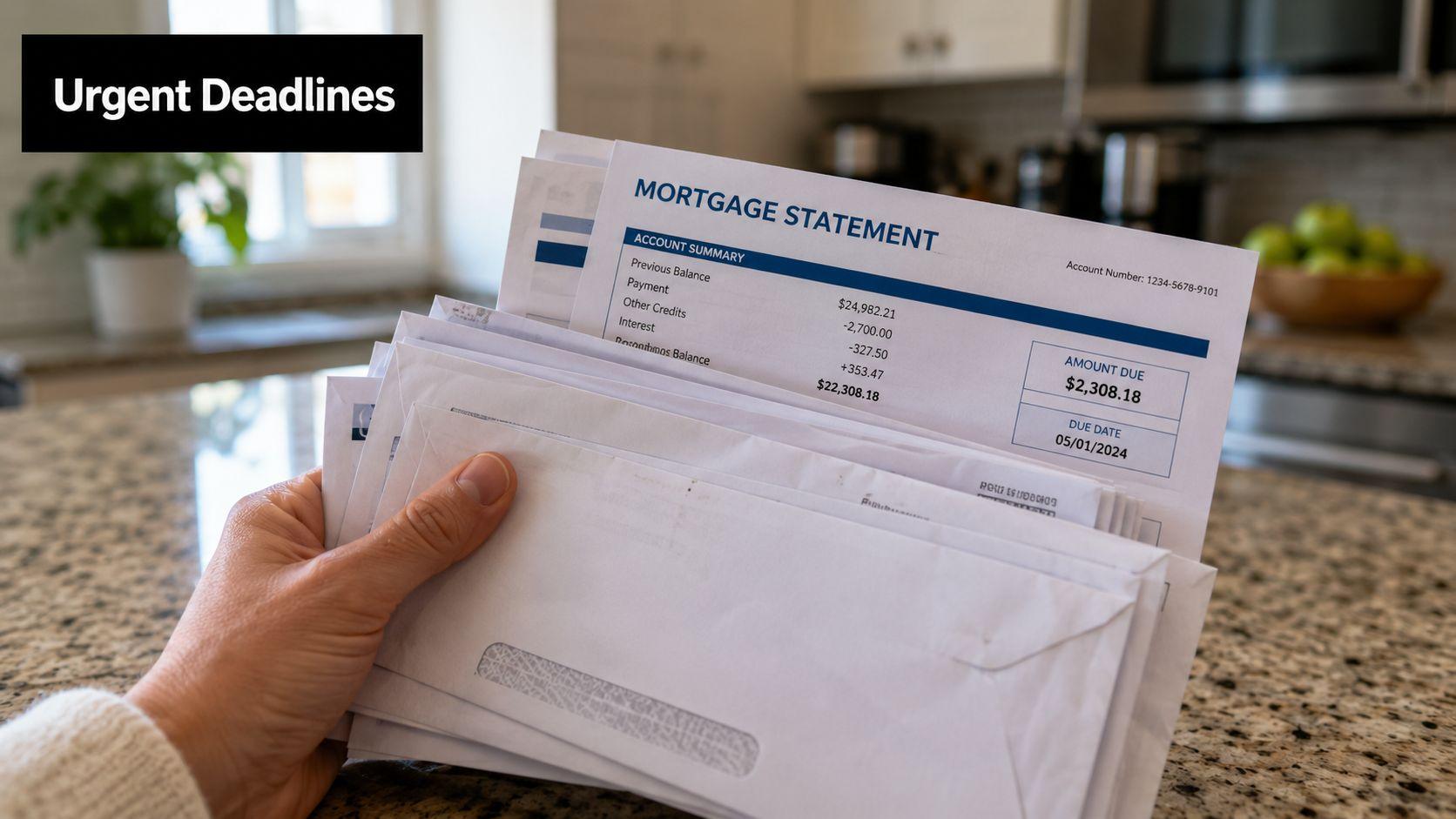

On day one, the house starts costing money whether the family is ready or not. In Miami-Dade and Broward, that pressure builds fast because the mortgage servicer, insurer, tax collector, and association all operate on their own timelines.

The first 30 days are about triage. Keep the property from slipping into default, keep insurance from lapsing, and keep a vacant South Florida house from turning into a larger repair bill. Families often lose time arguing about whether to keep the home, while the past-due notices keep coming.

The bills that can't wait

Start with the charges that can damage the property, the title, or the sale timeline if they go unpaid.

- Mortgage payment: Confirm the amount due, the grace period, and whether the loan was already delinquent before death.

- Homeowners insurance: Florida carriers care about vacancy, roof condition, water losses, and occupancy status. If the home is empty and the policy still reads like an owner-occupied residence, that needs attention quickly.

- Property taxes: Unpaid taxes create a separate problem from the mortgage and can cloud your exit options later.

- HOA or condo dues: In South Florida, associations can add late fees, interest, special assessments, violation fines, and estoppel delays.

- Utilities and basic upkeep: Air conditioning, leak checks, lawn service, and pest control protect value. A shut-off house in August can develop mold and water damage faster than heirs expect.

If the loan was already behind before death, treat that as an immediate risk assessment, not a paperwork issue. Families dealing with an inherited property in default often need the same playbook as any owner who is behind on mortgage payments.

What to do in the first week

Call the mortgage servicer and report the death. Ask what documents they need, where to send them, and whether they will speak with the personal representative, successor in interest, or family contact. Then call the insurance carrier and ask a direct question: is the home properly insured in its current condition and occupancy status?

After that, contact the HOA or condo association. In Broward and Miami-Dade, I have seen associations become the immediate headache because they control gate access, violation notices, parking, applications, and estoppel information needed for a sale.

Gather these documents right away:

- Death certificate

- Will or trust documents, if they exist

- Any probate filing papers

- Recent mortgage statements

- Insurance declarations page

- HOA or condo account statements

- Utility login information, keys, alarm codes, and mailbox access

If nobody has authority to act yet, the servicer may limit what it shares. The bills still keep running.

South Florida costs heirs often miss

The mortgage is only one part of the monthly burn rate. In 2026, many heirs in Miami-Dade and Broward are getting hit by rising insurance premiums, association special assessments, and deferred maintenance that was manageable for the deceased owner but does not make sense for the estate.

That is the trade-off in the first month. If the house has strong equity and decent condition, paying to stabilize it may be the smart move. If it has an old roof, active leaks, unpaid condo dues, or a loan already in trouble, the family needs to calculate whether holding the property for probate is worth the cash outlay.

Stabilize the house itself

Walk the property as soon as you can. Check for roof leaks, ceiling stains, plumbing drips, broken windows, signs of occupancy, and whether the air conditioning is working. Photograph every room and exterior elevation. That record helps with insurance, family disputes, and sale planning.

Change the locks if the estate has authority and confirm who is living there. An inherited house in South Florida may have a relative, tenant, caregiver, or unauthorized occupant in possession. That affects insurance coverage, repair access, and whether a fast as-is sale is even possible.

For families comparing how debts are handled in other probate situations, this overview of debt after death in Texas is useful because it shows the same basic rule. The debt does not disappear because the owner died, and secured property still needs active management while the estate is being sorted out.

Understanding Your Legal Rights with an Inherited Mortgage

The most important legal distinction is this. You can inherit the property without automatically becoming personally liable for the deceased owner's mortgage debt.

The mortgage lien usually survives and stays attached to the property. That means the lender can pursue the house if payments stop. But unless you formally assume the loan, the lender's claim is generally against the property itself, not your personal assets, as described in this explanation of inherited mortgage liability and probate cash-flow planning from Harrison Estate Law.

Title is not the same as personal liability

This distinction matters because many heirs panic and think receiving the house means receiving a new personal debt obligation. Usually, that's not how it works.

Here is the practical version:

- The house carries the lien

- The lender wants the payments to continue

- The heir doesn't automatically step into full personal borrower liability

- The property can still be lost if nobody performs

That difference gives you room to decide. You can evaluate whether to keep the house, market it, refinance later, or resolve it through the estate without assuming that your own bank account is instantly on the hook.

Federal protection most heirs don't realize they have

The federal Garn-St. Germain Depository Institutions Act of 1982 limits lenders from enforcing due-on-sale clauses when property is transferred to certain relatives after death. That means a qualifying heir can often continue making payments on the existing mortgage rather than being forced into immediate payoff or refinance, as summarized in this AllLaw discussion of inherited real estate and mortgage transfers.

That federal protection is the reason many inherited homes in Florida remain workable even when the loan is still active.

The lender may still require paperwork. It usually can't simply force a qualifying heir into a brand-new loan because the owner died.

Families often get tripped up by this misunderstanding. They hear “you can keep paying” and assume the servicer will make it easy. It usually doesn't.

The successor-in-interest bottleneck

Servicers want documents before they discuss loan status in detail. If you need a broad overview of exit paths before deciding whether to keep the property, this guide on ways to get out of your mortgage legally gives a useful framework.

In inherited-house files, the problem is rarely just the rule. The problem is the delay between the rule and the paperwork. Until the servicer recognizes the right person, loan access, modification requests, reinstatement discussions, and payoff coordination can all slow down.

In Miami-Dade condos and Broward subdivisions, that delay can collide with association deadlines and insurance issues. Legal rights matter. So does getting recognized fast enough to use them.

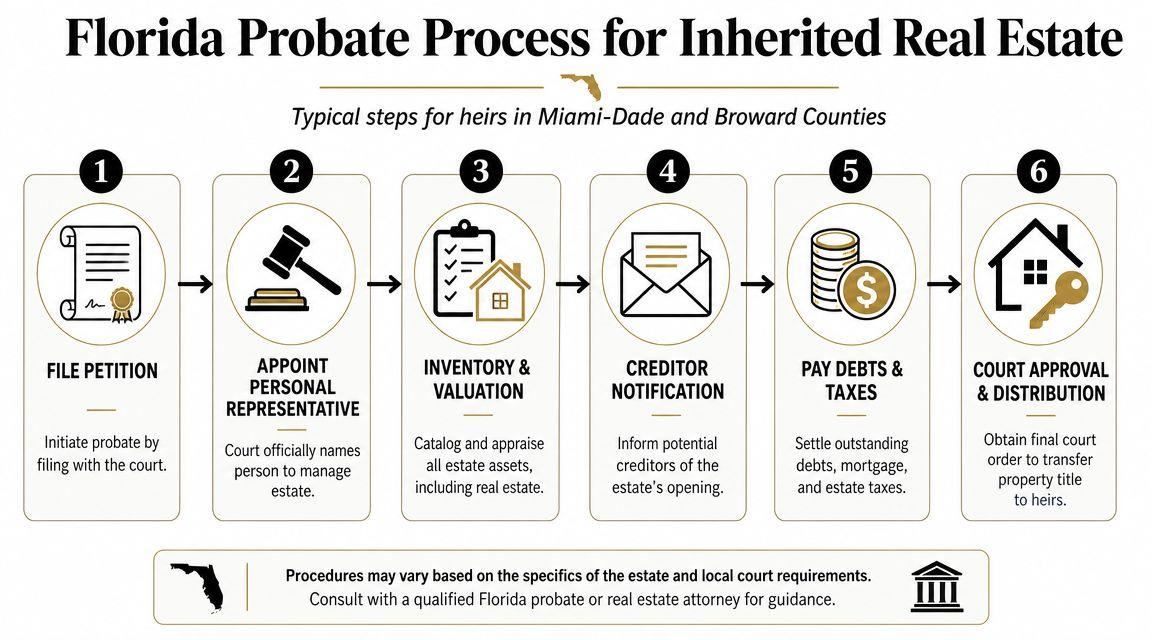

How Florida Probate Impacts the Inherited House

In Florida, the house doesn't move cleanly from the deceased owner to the heirs just because everyone in the family agrees. Authority comes from the probate process unless the property passed outside probate through a trust, enhanced life estate deed, or another non-probate transfer method.

For a mortgaged house, the court process matters because someone needs legal power to collect records, manage the asset, pay carrying costs, and if necessary sign a sale contract and closing documents.

The personal representative controls the file

In most Florida probate cases involving a house with an active mortgage, the court appoints a Personal Representative. That person acts for the estate after the court issues Letters of Administration.

Without those letters, families often run into the same problem repeatedly. Everyone knows what should happen, but the bank, title company, and closing agent need proof of who can act.

Typical duties include:

- Securing the property

- Inventorying the estate asset

- Dealing with the mortgage servicer

- Handling creditor issues

- Maintaining insurance and taxes

- Coordinating a transfer or sale

Formal administration usually drives the timeline

In practice, a Florida house with a mortgage often ends up in formal administration because there is an active debt, active title work, and usually a need for broader authority. Families sometimes ask whether they can avoid the heavier probate process, but the answer depends on how title was held and what else is in the estate.

The local court process also isn't identical in feel from county to county. Miami-Dade probate files often involve more layered title issues, condo documentation, and out-of-state heirs. Broward probate files often run into association compliance, homestead history, or vacancy-condition problems that affect insurability and marketability.

In probate, delay has a carrying cost. Every extra month can mean another mortgage payment, another insurance premium, another HOA invoice, and another maintenance problem.

During probate, principal, interest, taxes, and insurance still have to be paid to avoid default, and the heir is typically not personally liable for the mortgage debt unless the loan is formally assumed. The lender's claim is generally in rem against the property, not automatically against the beneficiary's personal assets, as noted earlier in the legal discussion.

Selling during probate in Florida

Selling an inherited house in probate is often straightforward only after the right authority is in place and title issues are understood. If you need a practical overview of timing, documents, and sale logistics, this resource on how to sell inherited property covers the actual-world sequence well.

The point most families miss is that probate isn't just a legal container. It affects negotiation advantage. If the house needs repairs, has unpaid association balances, or sits in a building with aggressive condo rules, every delay narrows your options.

Decision Framework Keep Sell or Walk Away

Most heirs don't need more theory. They need a decision standard.

The right choice depends on four things. Whether the property has workable equity. Whether someone in the family can carry the monthly costs. Whether the title and probate path are clean enough to support a sale or refinance. And whether the house itself is physically manageable in the current Florida insurance and HOA environment.

Comparing Your Options for an Inherited House

| Factor | Keep the House (Assume/Refinance) | Sell on Open Market | Sell for Cash to Property Nation |

|---|---|---|---|

| Best fit | You want to live in it or hold it long term | You want market exposure and can tolerate prep time | You want speed, certainty, and an as-is exit |

| Mortgage handling | Continue payments and coordinate with servicer | Keep loan current until closing | Resolve loan through a direct sale process |

| Repairs | You take them on over time | Usually some prep is needed to compete | Typically sold as-is |

| Cleanout | You manage it | Usually needed before listing photos and showings | Often flexible for heirs still sorting belongings |

| Timeline | Depends on probate, servicer cooperation, and affordability | Depends on probate, property condition, and buyer financing | Built for probate sellers who need a simpler path |

| Carrying costs | Ongoing mortgage, taxes, insurance, HOA, maintenance | Continue until closing | Shorter exposure to ongoing carrying costs |

| Emotional burden | Highest if the house needs work or family coordination | Moderate to high because of showings and negotiations | Often lowest because the process is more contained |

| Upside | Keep a family asset | Potentially strongest retail pricing | Fast resolution with fewer moving parts |

| Main risk | Becoming house-rich and cash-poor | Delays, repairs, inspection demands, financing fallout | Accepting convenience over a full retail listing strategy |

One useful outside overview for families sorting through procedure is this guide on navigating Florida estate probate. It helps clarify why good decisions on inherited property depend so heavily on who has authority and when.

When keeping the house works

Keeping the property makes sense when one heir wants to occupy it, the monthly obligations are sustainable, and the house isn't sitting on hidden problems like deferred roof work, major association disputes, or vacancy-related insurance trouble.

In South Florida, I tell relatives to pressure-test ownership with one question. Would you buy this exact house today, in this condition, with these carrying costs, from a stranger? If the answer is no, sentiment may be disguising a bad hold.

When selling conventionally works

A retail sale can be smart when the home is in presentable condition, the heirs can wait through probate and marketing, and there is enough cooperation among family members to handle cleanout, access, inspections, and buyer demands.

This path breaks down when the house is cluttered, dated, vacant, leak-damaged, or in a condo building with strict access and document issues.

A short video can help frame the mindset around inherited-property choices before you commit to a path.

When walking away becomes rational

Walking away isn't the first choice. Sometimes it's the cleanest one.

If the property is underwater, physically distressed, or burdened by more problems than value, heirs may decide not to keep feeding it cash. In those cases, the analysis turns on whether there is real equity to preserve, whether a short sale is possible, or whether surrendering the property is better than funding a losing asset during probate.

The Fast-Track Solution Selling Your Inherited House for Cash

Some inherited homes don't need a longer decision tree. They need closure.

That is usually true when the property has one or more South Florida stress points at the same time. A nonpaying occupant. A condo association that keeps sending violations. An older roof that scares insurers. A house full of personal belongings. A family spread across states that can't coordinate repairs, listing prep, and probate timing.

Why an as-is sale changes the equation

A direct cash sale removes the parts of the process that usually exhaust heirs.

- No repair cycle: You don't have to patch drywall, replace flooring, or chase contractors before the house can move.

- No staging or repeated showings: That matters when the home is still full of a relative's belongings.

- No financing uncertainty: The sale is not waiting on a buyer's loan approval or appraisal drama.

- No long carrying period: Less time owning the house means less exposure to mortgage, taxes, insurance, and association costs.

If speed is the priority, this guide on how to sell your house in 7 days or less captures why direct-sale timelines appeal to probate families under pressure.

What this looks like in Miami-Dade and Broward

In Miami-Dade, inherited properties often come with condo rules, older interiors, and document-heavy closings. In Broward, vacant single-family homes often raise maintenance and insurance problems first. In both counties, families usually underestimate the labor involved in getting a house retail-ready after a death.

A clean, as-is exit often preserves more real value than a delayed retail plan that keeps bleeding money every month.

That doesn't mean a cash sale is always the best price on paper. It means some heirs value certainty more than theoretical upside. If the house needs work, the family is divided, or probate is already hard enough, reducing the number of moving parts is often the best financial decision available.

FAQ Inherited Mortgage Questions Answered

What if the house has a reverse mortgage

Treat a reverse mortgage as a short-fuse problem.

After the borrower dies, the loan usually becomes due. Heirs often have limited options. Sell the property, refinance into a new loan, or turn the house over if keeping it no longer makes financial sense. In practice, I tell Miami-Dade and Broward families to call the servicer early, ask for the payoff process in writing, and confirm every deadline. Reverse mortgage files can move faster than families expect, especially when the home is vacant.

If the property needs work, the timeline matters even more. A dated condo in Miami or an older Broward house with roof or insurance issues can lose time quickly while the estate is still getting organized.

What if multiple heirs disagree about whether to keep or sell

This is one of the most common probate fights in South Florida.

One heir wants to keep the house for sentimental reasons. Another wants their share of the equity now. A third cannot help with the mortgage, taxes, HOA dues, or insurance, but still objects to a sale. That standoff gets expensive fast. In Florida, the disagreement can turn into a buyout negotiation, a court fight inside probate, or a partition action after title is sorted out.

Put real numbers on the table early. Get the mortgage balance, monthly carrying costs, payoff amount, likely sale value, repair needs, and probate timeline. Once heirs see what the property is costing each month, the conversation usually becomes more practical.

What if the mortgage servicer won't talk to me

Usually, the servicer is waiting for proof that you have authority to receive loan information.

That may mean death certificates, probate paperwork, letters of administration, or documents showing you qualify as a successor in interest. Legal Aid NYC explains that heirs often have to make a written request and provide documentation before the servicer will fully discuss the loan or accept certain instructions, as outlined in this Legal Aid NYC overview of inheriting a home with a mortgage.

Do not wait for perfect paperwork before acting. Keep making any payment the estate intends to make, document every call, and send follow-up letters or secure messages. In Florida probate, delay is common. Late fees, force-placed insurance issues, and default notices do not pause just because the family is still gathering documents.

What if the house is worth less than the mortgage

Then sentiment cannot drive the decision.

Look at the full picture: loan payoff, arrears, attorney fees, taxes, HOA or condo balances, insurance, and the condition of the property. In Miami-Dade and Broward, association debt and insurance problems can wipe out thin equity much faster than families expect. If the numbers do not support keeping the house, the practical options are usually a short sale, deed in lieu, negotiated payoff, or letting the lender take the property.

I have seen families spend months trying to save an inherited house that had no real equity left. A fast, as-is sale can still be the cleanest exit if the lender will cooperate and the estate needs certainty more than a long shot at a higher price.

If you need a straightforward path for an inherited house in Miami-Dade or Broward, Property Nation helps heirs and personal representatives sell probate and inherited properties as-is, without repairs, showings, or cleanout pressure. When the goal is to stop the carrying costs, resolve the mortgage, and move the estate forward, a local cash-sale option can simplify the process dramatically.