Selling a home in South Florida gets stressful fast when the title isn't clean. A Miami-Dade condo sale can slow down over an HOA estoppel issue. A Broward inherited house can sit in limbo because the owner of record passed away and probate was never finished. A cash buyer may be ready, but the deed, payoff, legal description, or signature package still has to line up before ownership can transfer.

That's the part many homeowners don't see coming. The title transfer process isn't just signing at closing. It's the legal handoff of ownership, and in Florida that handoff depends on accurate documents, county recording, payoff coordination, and problem-solving when the file is anything other than routine. If you're trying to move quickly, a clean packet matters more than almost anything else.

Table of Contents

- Your At-a-Glance Guide to Florida Title Transfers

- Decoding Florida Deeds A Comparison of Transfer Documents

- The Title Transfer Timeline Step by Step

- Required Documents and Fees in Miami-Dade and Broward

- Common Complications That Stall Florida Home Sales

- The Fast-Track Solution for As-Is Sales

- Frequently Asked Questions about Florida Title Transfers

- Can I transfer a property title in Florida without a lawyer?

- Can I transfer title to a family member for $1?

- What is the difference between a title company and a real estate attorney in a Florida closing?

- Can I sell if my property is in probate?

- What usually delays title transfer the most in Miami-Dade and Broward?

Your At-a-Glance Guide to Florida Title Transfers

A lot of South Florida sellers call after they already have a buyer, a closing date, and a problem. The problem is usually title. A probate order is still pending. An heir expects to sign but has no legal authority. The condo association has not issued the estoppel letter. An old permit or lien surfaces once the title search starts.

In Florida, title transfer means legal ownership moves from seller to buyer through a properly executed deed, satisfaction of closing conditions, and recording in the county's official records. That sounds straightforward. In Miami-Dade and Broward, it often is not.

What matters most in practice

- The seller must have clear authority to sign: If the property is in probate, held in a trust, owned by an LLC with missing corporate records, or tied up in a divorce or foreclosure, the closing agent will stop the file until authority is proven.

- Small deed errors cause real delays: Misspelled names, a bad legal description, an incorrect marital status, or inconsistent vesting can trigger recorder rejection or force corrective documents after closing.

- A complete file shortens the review cycle: Florida closings move faster when payoff statements, death certificates, probate paperwork, HOA or condo estoppels, and government-issued ID are collected early instead of one item at a time.

- Local issues slow South Florida deals: In Miami-Dade and Broward, common hold-ups include association approvals, estoppel balances, municipal lien searches, open permits, code enforcement issues, and buyer concerns tied to 2026 insurance costs and roof history.

- The deed matters because the warranty matters: The transfer document does more than move title. It also defines what the seller is promising about prior claims and defects.

- Fast closings happen when title work starts first: Cash sales can close quickly, but only if liens, payoffs, ownership documents, and association requests are ordered at the start.

One practical rule saves sellers time and money. If the sale looks simple but the ownership story is messy, treat it as a title issue first.

That is especially true with inherited property. Under current Florida practice in 2026, a house does not become marketable for sale just because the family agrees on who should get it. The personal representative may need court authority. Homestead issues can affect who inherited. If one heir is missing or refusing to cooperate, the delay is legal, not logistical.

For homeowners who want a broader sale-prep roadmap before diving into title details, Property Nation's guide on selling a house in Florida is a useful starting point. For document flow and signatures, digital checklist tools such as BoloSign for property transactions can help keep the closing package organized instead of scattered across email threads.

Decoding Florida Deeds A Comparison of Transfer Documents

The deed is the legal instrument that transfers ownership. Sellers in Miami-Dade and Broward usually hear deed names tossed around as if they're interchangeable. They aren't. The deed form controls what the seller is guaranteeing, and that affects future liability.

A buyer purchasing on the open market usually expects stronger title assurances than a child receiving a parent's interest in a family property. That's why the “right” deed depends on the deal, the relationship between the parties, and whether the transfer is a sale, estate move, divorce cleanup, or title correction.

Florida Deed Types Compared

| Deed Type | Seller's Guarantee (Covenants) | Best Use Case | Seller Risk Level |

|---|---|---|---|

| General Warranty Deed | Broad promise that title is good and defensible against claims, including issues arising before the seller owned the property | Standard arms-length sale where buyer expects maximum protection | High |

| Special Warranty Deed | Limited promise covering title issues that arose only during the seller's period of ownership | Certain investor, estate, or entity sales where seller won't guarantee older title history | Moderate |

| Quitclaim Deed | No warranty of clear title. Transfers whatever interest the seller has, if any | Family transfers, divorce, trust transfers, or curing some title defects | Low on warranty exposure, high on buyer risk |

What each deed means for you as a seller

A General Warranty Deed gives the buyer the most comfort. It also gives the seller the broadest ongoing exposure if a title problem surfaces later. In a normal retail sale, this is common because buyer lenders and title underwriters want the strongest form of conveyance.

A Special Warranty Deed narrows the seller's promise. It says, in effect, “I'm standing behind my ownership period, not the entire chain before me.” That can make sense in estate administration, trustee sales, or some investment dispositions.

A Quitclaim Deed is fast, but speed doesn't equal protection. It transfers whatever ownership interest the grantor has without promising that the interest is valid, complete, or free of problems. That's why it fits low-conflict transfers between parties who already trust each other or where the goal is to correct title, not market the property to a stranger.

A quitclaim deed can solve an internal ownership issue. It usually doesn't solve a marketability issue by itself.

What works and what doesn't

What works is matching the deed to the transaction. Family settlement? Quitclaim might be enough. Open-market sale of a Broward single-family home? Buyers and closing agents typically want stronger assurances.

What doesn't work is copying a deed form from another situation and assuming it will carry a financed or contested closing. If you're unsure what deed fits your file, review the transfer documents and ownership structure before signing anything. Property-specific forms and closing paperwork are easier to understand when you've seen examples, which is why these real estate forms help many sellers ask better questions before closing.

The Title Transfer Timeline Step by Step

A seller in Miami Gardens signs a cash contract on Monday and expects to close by next week. Then the title search shows a probate issue, the HOA has not issued the estoppel letter, and an old permit was never closed out. That is how a "fast" sale turns into a delay.

The title transfer process moves as fast as the slowest unresolved item in the file. A clean cash sale can move quickly. A financed sale, probate property, condo unit, or distressed home usually takes longer because more documents, approvals, and payoff items have to line up before closing.

The file opens after the contract is signed

After the contract is fully executed, the closing agent or title company orders the title search, confirms current ownership, pulls tax information, and requests mortgage payoff figures if there is a loan. In Miami-Dade and Broward, good closers also start checking association requirements, municipal records, and whether the seller named in the contract matches the vesting on title.

Small errors cause real delays. A missing suffix, a prior spouse still shown in the chain, or a trust that never received title can force corrected documents and fresh signatures later.

The title review shows what has to be fixed before closing

The title search is looking for anything that prevents clean transfer. That includes unreleased mortgages, judgment liens, probate gaps, legal description mistakes, boundary issues, and breaks in the ownership chain.

Florida files do not stall because of one dramatic problem every time. They often stall because several minor issues stack up. One missing satisfaction, one unreadable prior deed, or one seller without clear signing authority is enough to hold recording until the file is corrected.

In Miami-Dade and Broward, delays usually happen before anyone signs

Local files tend to slow down in a few predictable places:

- HOA and condo estoppels: Associations may take time to issue estoppel letters, and unpaid balances, special assessments, or violation notices have to be resolved.

- Permits and code issues: Open permits, unsafe structure notices, and municipal liens can trigger additional review or buyer objections.

- Probate and inherited property: If the owner has died, the title company needs the probate file, homestead status, and authority for the personal representative or heirs to convey.

- Insurance-driven buyer concerns: Under Florida's 2026 insurance pressure, buyers and lenders look harder at roof age, prior claims, and property condition, especially on older South Florida homes.

- Foreclosure or distress: Active foreclosure, loss mitigation, or multiple payoff demands require precise coordination because the lien numbers have to match the closing figures.

Recording the deed is the last visible step. The harder work is clearing everything that can stop that recording.

Closing and recording

Once the title issues are cleared, the seller signs the deed and closing affidavits, the buyer sends funds, and liens are paid from closing proceeds. The deed is then submitted for recording in the county where the property sits.

In practice, recording is usually the easy part. Getting to a recordable deed is what takes time. If the paperwork is accurate and the authority to sign is clear, the transfer can move smoothly. If the file involves probate, a contested estate, association debt, or last-minute payoff problems, the timeline expands fast.

For sellers who need certainty more than top-market pricing, that trade-off matters. A direct cash sale often works because the buyer can accept condition issues, move faster on title objections, and close without waiting on lender underwriting, provided the legal authority to sell is in place.

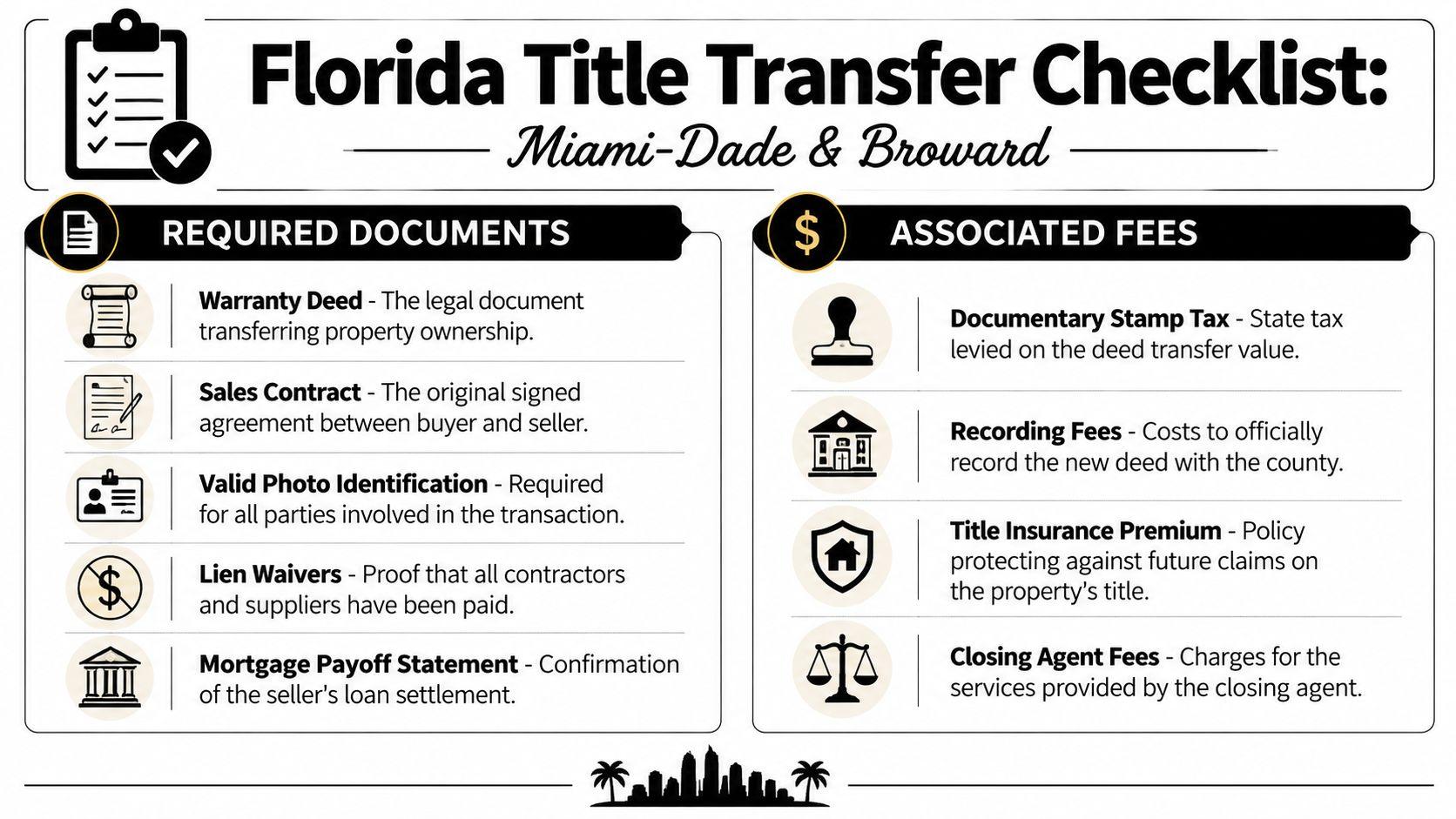

Required Documents and Fees in Miami-Dade and Broward

A lot of South Florida closings do not get delayed because the seller refused to sign. They get delayed because one line on the deed, one missing association estoppel, or one unresolved payoff item does not match the rest of the file. In Miami-Dade and Broward, that is common on inherited homes, condos, older properties with prior corrective deeds, and houses carrying open permits or lien questions.

The document stack sellers usually need

The closing agent or title company usually asks for a core set of documents early, then adds more if the ownership history is messy. Sellers in Miami-Dade and Broward should expect to provide most of the following:

- Executed deed: Usually a warranty deed, special warranty deed, or another deed that fits the transaction and vesting.

- Signed purchase contract: Used to confirm the parties, price, credits, deadlines, and closing instructions.

- Government identification: The name on the ID should line up with the deed and title commitment.

- Mortgage payoff information: Current loan numbers, servicer details, and authorization to obtain a payoff.

- Affidavits and supporting certifications: Common examples include name affidavits, marital status affidavits, trust certificates, entity authority documents, probate orders, death certificates, or other estate paperwork.

- Association and condo documents: Estoppel letters matter in this market. In many condo and HOA sales, the estoppel controls whether the closer can confirm balances, transfer approval issues, and money due at closing.

- Lien, permit, or violation backup: Releases, satisfactions, municipal lien searches, permit closures, or corrective instruments may be needed before recording. Sellers dealing with claims against the property should understand how selling a house with a lien on it affects timing and net proceeds.

Condo sellers should pay special attention to association paperwork in 2026. Between tighter budgets, deferred maintenance pressure, and insurance-related scrutiny, associations are slower to issue complete responses than many owners expect. If the estoppel is late or incomplete, the closing date can slip even when the deed itself is ready.

The fields that can get a deed rejected

County recording offices focus on accuracy, not intent. The deed has to match the ownership record and the rest of the closing file. The high-risk fields are the legal names of the parties, vesting language, legal description, parcel reference, execution details, and documentary stamp tax calculation.

Small errors create outsized problems. A missing suffix, a wrong unit number, an outdated legal description copied from an old deed, or a signer using the wrong representative capacity can force a correction before recording. I see this most often with inherited property, trust-owned property, and older Broward homes that have been refinanced or deed-corrected multiple times.

Fees sellers should expect

Sellers often budget for recording and overlook the rest of the closing charges. In Miami-Dade and Broward, the total cost usually includes several separate items:

- Documentary stamp tax on the deed

- Recording charges

- Title search and title insurance-related costs

- Settlement or closing fees

- HOA or condo estoppel charges

- Municipal lien search or permit-related charges

- Payoff statement fees, wire fees, or rush processing fees

- Corrective document costs if a title defect has to be fixed before closing

The practical issue is not just the amount. It is whether the numbers arrive early enough to keep the deal on schedule. An HOA can issue a revised estoppel. A lender can update a payoff through a specific date. A city or county search can show an old open permit the seller thought was closed years ago. Those are the line items that change a seller's net sheet at the last minute.

In Florida, fees also vary depending on how title is held, whether the property is homestead, whether there is a trust or estate involved, and whether the sale requires extra curative work before the deed can record. Sellers who need speed should ask for these items at the start, not the week of closing.

Common Complications That Stall Florida Home Sales

A clean title transfer process is straightforward. Most stalled sales aren't failing because the parties changed their minds. They're failing because the file has an exception that nobody addressed early enough.

Liens judgments and payoff surprises

Liens stop deals because clear title can't pass until valid claims are paid, released, bonded off, or otherwise resolved. In South Florida, that may involve mortgage liens, contractor claims, code enforcement issues, utility balances, judgment liens, or association claims.

The practical problem isn't always the lien itself. It's the missing release, old payoff mismatch, or disputed amount. A seller may think a debt was handled years ago, but if the public record still shows an unreleased claim, the closing agent will treat it as active until proven otherwise.

Probate and inherited property

If the owner of record has died, the title transfer process changes immediately. Heirs often assume a will alone lets them sell. It usually doesn't. The closer needs legal authority from the estate process or another valid vesting mechanism before a deed can transfer marketable title.

This is one of the biggest pain points in Broward and Miami-Dade inherited sales. One sibling wants to sell. Another is out of state. The home may still have a mortgage, unpaid taxes, or a vacant-property insurance problem. Until authority and heirship are squared away, the file stays stuck.

Probate problems don't just delay the deed. They delay every related item, including payoffs, affidavits, and buyer underwriting.

Foreclosure notices and distressed ownership

A pending foreclosure doesn't automatically block a sale, but it changes the pressure on timing and title clearance. If a lis pendens has been filed or default amounts are rising, the seller has less room for slow underwriting, buyer hesitation, or repeated document corrections.

In practice, distressed sellers often face multiple stacked issues at once. The house may need repairs that make financing harder. Insurance concerns may narrow the buyer pool. The mortgage payoff may be tight. There may also be association balances or municipal compliance items in the background.

Tenants easements errors and document defects

Occupied property can still transfer, but tenants create operational friction. Lease terms, access limits, security deposit credits, and buyer expectations all have to align. If the tenant is uncooperative, inspections and walkthroughs become harder, which can slow down buyer performance even when title itself is technically clear.

Then there are pure paperwork defects. Alterations, inconsistent signatures, incorrect sale prices, unresolved probate items, and missing releases can push a transfer into weeks or months of cleanup. Official guidance in transfer systems shows that errors, mark-throughs, and mismatched records often require affidavits, corrected filings, or other exception handling rather than a simple checklist fix, as described in this discussion of transfer defects and edge cases.

For sellers dealing with recorded claims, selling a house with a lien on it becomes less about whether a sale is possible and more about whether the payoff, release, and timing can be coordinated correctly.

The Fast-Track Solution for As-Is Sales

When a property has title friction, the conventional listing route often adds more moving parts. Showings start before the authority documents are ready. A financed buyer enters the file before the condo paperwork is complete. Inspection demands land on a house the seller already knows won't meet a retail buyer's comfort level without repairs.

A faster path is often an as-is cash sale structured around the title issue instead of pretending it doesn't exist. That means opening title immediately, identifying curative items early, and building the closing around probate authority, payoff coordination, association demands, or tenant occupancy rather than waiting for those problems to explode at the end.

What works better in distressed files

- Early title review: Open title before spending energy on cosmetic prep.

- As-is pricing logic: If the property has insurance, repair, or occupancy complications, structure the sale around current condition.

- Problem-specific closing coordination: Probate files need legal authority. Lien files need payoff strategy. Tenant files need access planning.

- Flexible closing dates: Sellers in foreclosure or estate administration often need control over timing more than anything else.

One local option is Property Nation's as-is home sale process, which is built around direct cash purchases, seller-selected timing, and closing coordination for situations like inherited property, liens, tenant issues, or houses that won't present well for a traditional listing. That model doesn't eliminate legal title requirements. It does reduce the number of consumer-facing obstacles around inspections, financing, repairs, and repeated buyer renegotiation.

What doesn't work is hoping a messy file will somehow become simple once a buyer appears. In South Florida, title problems usually get more expensive the longer they sit.

Frequently Asked Questions about Florida Title Transfers

Can I transfer a property title in Florida without a lawyer?

Sometimes, yes. But whether you should depends on the file. A routine transfer between informed parties may close through a title company or settlement agent. A probate transfer, disputed ownership file, trust issue, foreclosure-related sale, or deed correction usually benefits from legal review because one bad deed can create a much bigger problem later.

Can I transfer title to a family member for $1?

You can transfer property to family with a deed, but the deed choice, documentary tax treatment, mortgage consequences, and homestead implications still need review. The low stated consideration doesn't erase title requirements. If there's an existing loan, due-on-sale concerns and lender consent may matter.

What is the difference between a title company and a real estate attorney in a Florida closing?

A title company usually handles the title search, commitment, escrow, payoff coordination, and recording workflow. A real estate attorney gives legal advice, drafts or reviews legal documents with an advocacy role, and addresses disputed or complex legal issues. In a routine sale, the title side may carry most of the process. In a contested or inherited property sale, attorney involvement often becomes more important.

Can I sell if my property is in probate?

Often yes, but only once the correct estate authority is in place or the transaction is structured around the probate process. The person signing must have legal power to convey the property. If that authority is missing, the deed won't solve the problem.

What usually delays title transfer the most in Miami-Dade and Broward?

In practice, delays often come from probate authority, unresolved liens, association estoppels, open permit or municipal issues, tenant access problems, and deed preparation errors. Most of these are fixable. They just need to be identified early.

If you need to sell a South Florida property with title issues, inherited ownership questions, liens, tenant complications, or an as-is condition problem, Property Nation is a local resource for homeowners who want a direct sale path with fewer moving parts and a closing timeline built around the actual file, not an idealized one.