If you're in Miami-Dade or Broward right now, the pressure usually doesn't arrive from one problem. It piles up. The mortgage payment is already tight. Insurance renews at a number that doesn't make sense. The HOA starts sending violation letters or a special assessment notice. Then an inherited house, a vacancy, a tenant issue, or a missed payment turns a stressful situation into a legal one.

A florida short sale can be a real exit path when you owe more than the property can sell for. It isn't quick, and it isn't simple, but it can be better than letting a foreclosure case control the timeline. The hard part is knowing when a short sale is still workable and when the delays, lender review, and documentation burden make another solution more practical.

This guide is written for homeowners dealing with real South Florida issues in 2026. Miami-Dade and Broward owners aren't just facing market softness. They're facing insurance shock, aggressive HOA enforcement, probate delays, title problems, and the very real risk that waiting too long removes options. If you're already missing payments, this overview of what happens if you can't pay your mortgage helps frame the urgency before the lender does it for you.

Table of Contents

- At-a-Glance What is a Florida Short Sale in 2026

- Understanding Florida Short Sale Eligibility

- The Lender Approval Process and Timeline

- Short Sale vs Foreclosure vs Cash Sale A Comparison

- Florida's Legal and Tax Implications in 2026

- Common Pitfalls and 2026 Market Headwinds

- Florida Short Sale FAQs

At-a-Glance What is a Florida Short Sale in 2026

A florida short sale is a sale where the lender agrees to accept less than the full mortgage payoff so the property can be sold before foreclosure. You don't get to make that call on your own. The bank has to approve the reduced payoff because the sale proceeds won't fully cover the debt.

This isn't a niche issue anymore. In Q1 2025, Florida single-family short sales rose 32.8% year over year, according to Florida Realtors' statewide single-family summary. That matters in 2026 because more owners are finding themselves squeezed between older mortgage balances and current carrying costs that no longer fit their income.

In South Florida, the homeowners who call about short sales usually fall into a few categories. Some bought or refinanced when values were higher and now don't have enough equity to sell conventionally. Others could still make the mortgage for a while, but the full monthly cost of ownership has changed because insurance, HOA charges, maintenance, and legal issues around the property have changed.

What makes 2026 different

Miami-Dade and Broward owners are dealing with a version of distress that isn't always obvious from the outside. A homeowner can still be employed and still be in trouble. A condo owner can be current on the loan and still have no practical path forward because of insurance increases, assessments, or building-related costs.

A short sale is often less about one missed payment and more about proving the property no longer works as a sustainable asset.

A short sale can help you avoid a foreclosure judgment and regain some control over the exit. But it also comes with lender review, paperwork, delays, and uncertainty. That's why the first question isn't "Can I do a short sale?" It's "Does a short sale still fit my timeline, risk level, and property condition?"

Understanding Florida Short Sale Eligibility

Most rejected files fail for a simple reason. The owner knows they're in a bind, but the lender doesn't have enough evidence to approve the loss.

The two things the lender must see

The foundation of a florida short sale is negative equity and hardship. The core package has to prove both, using a hardship letter, financial statements, and a Broker's Price Opinion that relies on 3 to 6 recent comparable sales, as explained in this breakdown of Florida short sale package requirements.

Negative equity means the property's current market value is lower than the debt that has to be paid off. If the sale won't satisfy the mortgage, the lender has to decide whether taking less now is better than taking the property through foreclosure.

Hardship is the second pillar. In real life, that might be job loss, medical strain, divorce, reduced rental income, an inherited property you can't afford to maintain, or a payment structure that no longer works. In Broward and Miami-Dade, owners also run into hardship when the property itself becomes the problem. A vacant house deteriorates. A tenant stops cooperating. A condo starts generating recurring special costs. If you're already struggling, this guide on behind on mortgage payments in Florida is a useful reality check on how fast the file can escalate.

What a real short sale package includes

Lenders don't approve short sales because the seller is frustrated. They approve them because the package shows a documented loss scenario.

A workable file usually includes:

- A hardship letter that explains what changed, when it changed, and why the mortgage is no longer sustainable.

- Financial statements showing income, expenses, assets, debts, and available cash.

- Income and asset proof such as bank statements and tax records.

- A BPO or CMA using recent comparable sales that supports the current market value.

- A proposed settlement statement showing the lender what the net recovery looks like.

Practical rule: If the hardship letter is vague and the value support is weak, the lender will treat the file like a seller preference, not a hardship file.

Owners get into trouble when they submit a package that feels emotional but not documented. Banks aren't looking for a dramatic story. They're looking for a file that ties the hardship to the inability to carry the property and ties the price to current market evidence.

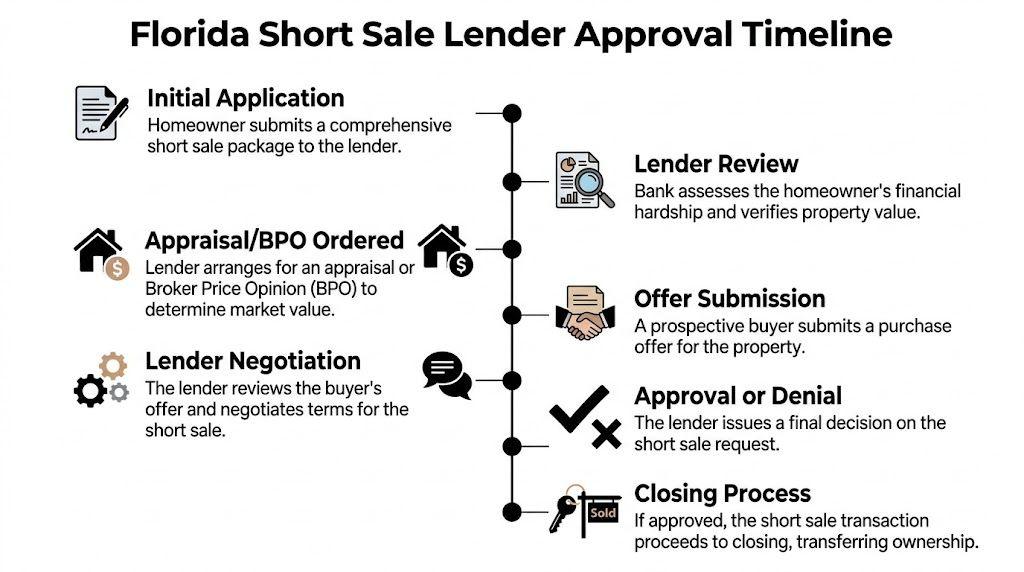

The Lender Approval Process and Timeline

The short sale process feels slow because it is slow. Everyone involved is waiting on someone else. The seller waits on the agent, the buyer waits on the lender, the lender waits on valuation, and the foreclosure clock often keeps running in the background.

To make the sequence easier to see, start with the full approval path:

How the timeline actually unfolds

Florida short sale timelines average 4 to 8 months, including 1 to 2 months for the seller's financial assessment, 30 to 60 days for the lender's initial response and valuation, 2 to 4 weeks for negotiation, and another 4 to 6 weeks to close, based on this overview of the Florida short sale approval timeline.

That timeline assumes the file is complete and the buyer stays in place.

The usual order looks like this:

File assembly

The seller and agent gather the hardship package, lien information, payoff data, and pricing support. Missing bank statements, outdated financials, and inconsistent hardship explanations create delays early.

Property goes active

The home is listed and marketed subject to lender approval. Buyers often ask whether the home can close on a normal schedule. The answer is usually no.

Offer submission

Once the seller accepts an offer, the package goes to the lender. The bank then evaluates hardship, property value, and net recovery.

Later in the process, many sellers find it helpful to hear the timeline discussed visually:

Where deals slow down

The most common stall points aren't mysterious. They're procedural.

- Valuation disputes. The lender's BPO may come in higher than the market will bear, especially if the house needs work or the comparable sales don't reflect current condition.

- Incomplete submissions. A single outdated statement or unsigned form can kick the file back into review.

- Junior liens and title issues. HOA balances, code enforcement liens, probate defects, or municipal issues can interrupt approval even after the first mortgage is engaged.

- Buyer fatigue. A buyer who was willing to wait at the beginning may not wait through repeated silence.

The short sale isn't approved when the seller accepts an offer. It's approved when the lender says yes in writing, with terms the closing agent can actually perform.

In Miami-Dade and Broward, this matters because distressed properties often carry more than one complication. The house may be in probate. The condo may have association issues. The title may show an old lien. Every added layer lengthens the file and increases the chance that the lender or buyer walks away.

Short Sale vs Foreclosure vs Cash Sale A Comparison

When homeowners feel cornered, they often compare only two outcomes, short sale or foreclosure. That misses the third path, a direct cash sale, which removes lender approval from the equation. The right choice depends on time, credit concerns, property condition, liens, and whether you can tolerate uncertainty.

Florida Homeowner Options Compared

| Factor | Florida Short Sale | Foreclosure | Cash Sale (Property Nation) |

|---|---|---|---|

| Who controls the timeline | Seller starts it, but lender controls approval | Lender and court control the case | Seller and buyer set the closing schedule |

| Typical pace | Extended. Lender review can take months | Unpredictable and court-driven | Fast and direct |

| Need for lender approval | Yes | Not applicable. The lender is enforcing the debt | No lender approval for the sale itself |

| Property condition expectations | Buyer and lender still care about value and condition | Property condition often worsens during the case | Sold as-is |

| Showings and listing process | Usually yes | Not a normal sale process | No traditional listing |

| Credit impact | Can be serious, but usually better than foreclosure | Typically the most damaging path | Depends on the owner's broader credit picture, but it doesn't carry the same short sale or foreclosure reporting issues |

| Outcome certainty | Moderate to low until written lender approval | High that the case proceeds if unresolved | High once contract terms are agreed |

| Deficiency risk | Possible if not waived in writing | Possible depending on the case and judgment | Not structured as debt forgiveness through lender approval |

| Fit for probate, liens, or tenant issues | Harder. Extra complexity can derail approval | Those issues often become more expensive over time | Often the cleanest path when the property has operational problems |

How to read the trade-offs

A short sale gives the seller some participation in the exit. That's the benefit. But the seller still has to satisfy a bank that may value the property differently, move slowly, or demand additional terms. If the home needs work, has HOA trouble, or sits in probate, that uncertainty gets worse.

Foreclosure is the least controlled outcome. The lender files the case, the court process takes over, and the owner's bargaining power shrinks as deadlines pass. Owners in this position often also stop maintaining the property because they don't know whether they should spend more money on a house they may lose anyway.

A direct cash sale is different because it isn't asking the lender to approve a discounted payoff as part of the sale structure. It's a straightforward purchase transaction. That's why owners who want to understand pricing often benefit from this explanation of how Florida cash home offers are calculated in 2026.

For Miami-Dade and Broward homeowners, the practical question is simple. If the property has enough time, clean enough paperwork, and a lender likely to cooperate, a short sale may be worth attempting. If the house has legal, title, tenant, or condition issues and the owner needs certainty, speed matters more than theoretical upside.

Florida's Legal and Tax Implications in 2026

The sale itself is only part of the problem. The approval letter, the deficiency language, and the tax consequences matter just as much as getting to the closing table.

Deficiency risk and approval language

In Florida, a lender may try to preserve the right to pursue the unpaid balance after a short sale unless the approval terms clearly waive that claim. That's why owners shouldn't treat lender approval as a simple green light. The exact wording matters.

Some homeowners assume a short sale automatically wipes out the remaining debt. It doesn't. The release has to be written into the approval structure or otherwise resolved with the lender. That issue becomes more sensitive when there are multiple loans, association balances, or other title complications.

Get the approval letter reviewed carefully. A short sale that closes but leaves unresolved liability can create a second problem after the first one ends.

Florida law can also affect whether a lender may pursue a deficiency judgment in a given case. The details depend on the loan documents, the property type, and how the resolution is documented. Owners dealing with both distress and longer-term holding costs should also think through adjacent costs, including taxes, which is why some review broader timing issues like Florida 2026 property tax changes and whether to sell now or wait.

Credit and tax questions

A short sale can still hurt credit. One verified source in the background materials notes a credit score deduction of 100 to 150 points as a possible outcome, but the broader point is more important than the exact figure. The impact is usually less severe than foreclosure, yet still meaningful.

Tax treatment is also case-specific. If a lender forgives debt, that forgiven amount may raise tax questions depending on the owner's circumstances and the status of applicable relief rules at the time of filing. Because this area changes and turns on individual facts, homeowners should get tax advice tied to the approval letter and the year of the transaction rather than relying on general internet summaries.

What works is precision. Owners need the hardship approved, the deficiency language addressed, and the tax reporting understood before closing, not after.

Common Pitfalls and 2026 Market Headwinds

In South Florida, many short sales don't start because the mortgage suddenly became unaffordable on its own. They start because the total cost of keeping the property changed faster than the owner expected.

Why South Florida owners are getting trapped faster

A key driver in 2026 is the rise in carrying costs. In South Florida, some homeowners insurance premiums have risen 40 to 50%, and rising HOA fees are also pushing owners toward proactive short sales, as discussed in this analysis of why short sales are making a comeback in Florida.

That creates a different kind of distress. A homeowner in Miami-Dade can be current on the mortgage and still have no sustainable exit except sale. A Broward condo owner can absorb the loan payment but fail on the combined burden of insurance, association charges, and special assessments.

For owners trying to understand the insurance side of the equation, this overview of South Florida flood insurance is a practical resource because flood exposure and premium structure often affect holding decisions long before a formal default.

What usually kills a workable short sale

The market isn't forgiving when the file is weak. These are the problems that show up repeatedly:

- An inexperienced listing strategy. If the property is priced without realistic condition adjustments, the lender may expect a number the market won't support.

- Waiting too long after the hardship is obvious. Once foreclosure counsel, HOA enforcement, or probate delays stack up, the short sale becomes harder to land.

- Poor property access or condition during marketing. Buyers don't wait forever, especially when the home has deferred maintenance or occupant issues.

- Underestimating HOA pressure. Associations in Miami-Dade and Broward can make an already distressed property much harder to sell cleanly.

- Treating probate like a side issue. If authority to sell isn't lined up, the bank may be ready before the estate is.

Some of the hardest files aren't the most underwater. They're the ones where insurance, HOA, title, and occupancy issues all collide at once.

The lesson is blunt. Speed matters more in 2026 because the carrying costs are rising while the paperwork burden isn't getting lighter.

Florida Short Sale FAQs

Can I short sell an inherited or probate property in Florida

Yes, sometimes. This is one of the most misunderstood florida short sale situations. Lenders may approve a proactive short sale on an inherited or probate property if the heir can prove hardship, such as an inability to cover the mortgage, upkeep, or related costs. But the process is risky because documentation delays and weak offers can sink the file, and DIY success rates can fall below 30%, according to this discussion of common short sale pitfalls for inherited and distressed properties.

If probate authority isn't clear, the sale can stall even when the lender is otherwise open to approval.

Do I have to be behind on my mortgage to qualify

Not always. Some lenders will review a proactive short sale if the hardship is real and documented. The key is showing that the property isn't financially sustainable, not just inconvenient. That often comes up with inherited houses, rentals with declining margins, or owners facing major insurance and HOA increases.

What happens if the bank rejects the short sale

The property doesn't automatically become unsellable, but that specific path is blocked unless the file changes. Sometimes the issue is value. Sometimes it's incomplete documentation. Sometimes the lender decides the expected recovery isn't strong enough.

When a short sale is denied, homeowners usually have to reassess quickly. That may mean improving the package, exploring another negotiated workout, or moving to a sale structure that doesn't depend on lender short sale approval.

Can I do a short sale if the property has liens or tenant issues

Possibly, but it gets harder. Liens complicate title clearance and tenant problems can affect access, buyer confidence, and valuation. Those aren't minor side issues. In South Florida, they're often the reason a file drifts from difficult into unworkable.

Is a short sale better than foreclosure

Often yes, especially if your goal is to avoid a foreclosure judgment and keep more control over the exit. But "better" doesn't always mean "best." For some owners, the lender timeline, documentation burden, and uncertainty make another sale path more practical.

If you're dealing with foreclosure pressure, HOA demands, probate complications, liens, tenants, or an inherited house that can't wait, Property Nation offers a direct cash sale option across Miami-Dade, Broward, and throughout Florida. You can request a no-obligation offer, sell the property as-is, skip repairs and showings, and choose a closing timeline that fits your situation.